Bank of England Didn't Suffer That Much From Black Wednesday

The short version of the United Kingdom’s Black Wednesday, otherwise known as the ERM Crisis, is that in 1992 Britain was part of the European Monetary System (EMS) along with other countries like Spain, Italy, Germany, and France. Part of that agreement required member countries to keep their currency at a certain level through what was called the Exchange Rate Mechanism (ERM).

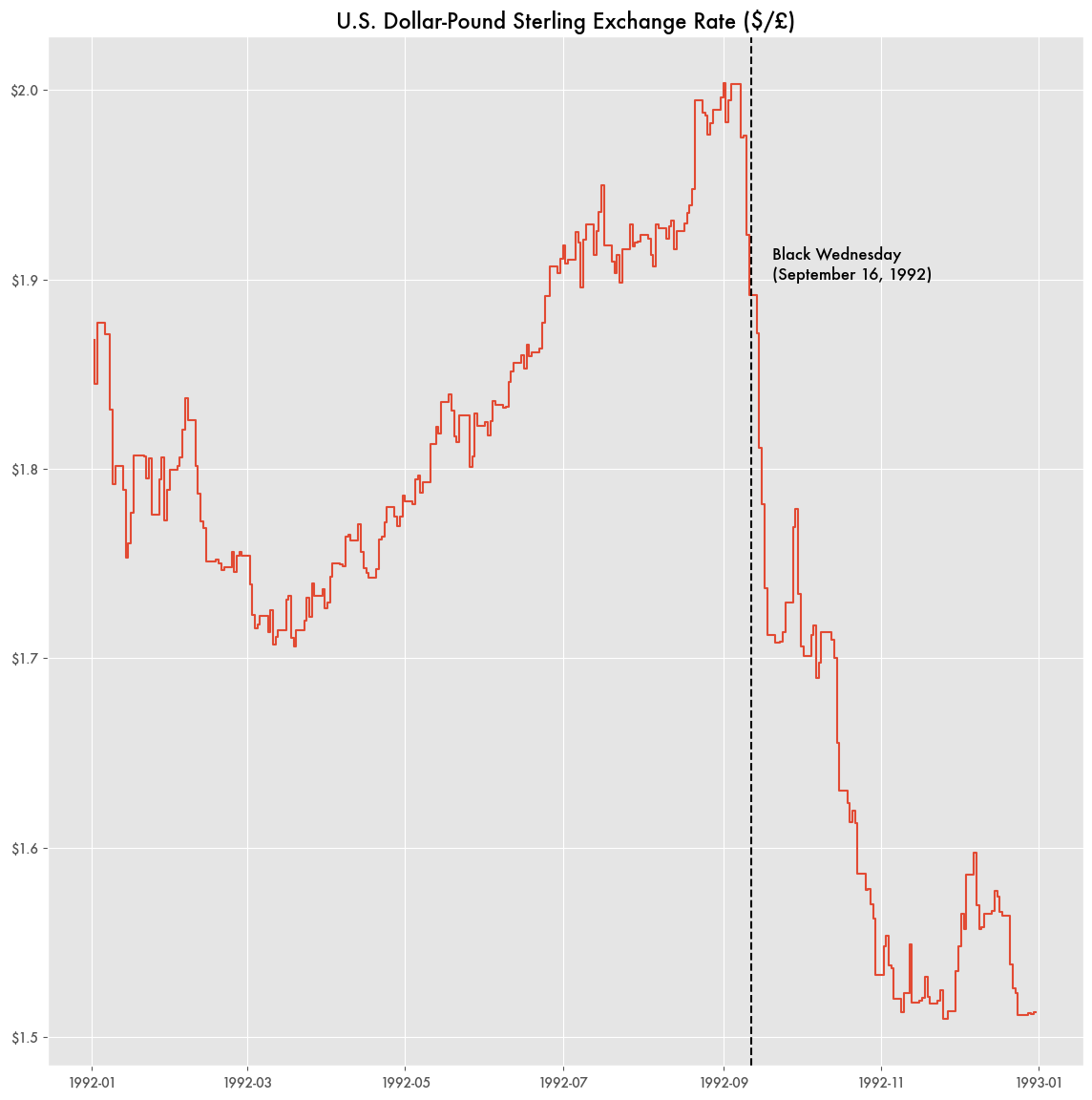

But the pound was overvalued, and, despite its best efforts, the Bank of England couldn’t prop up its value any longer. Currency speculators swooped in to bet against the pound, with George Soros’ Quantum Fund alone betting an incredible £10 billion on its collapse by borrowing and selling 61 percent of the pounds in circulation at the time (£16.4 billion). That bet would effectively earn him £1 billion in profit—possibly one of the largest single day windfalls in investment history. Britain’s attempt to join the EMS was abandoned and within a month sterling would lose 20 percent of its value.

Campaign to Drive Sterling’s Value

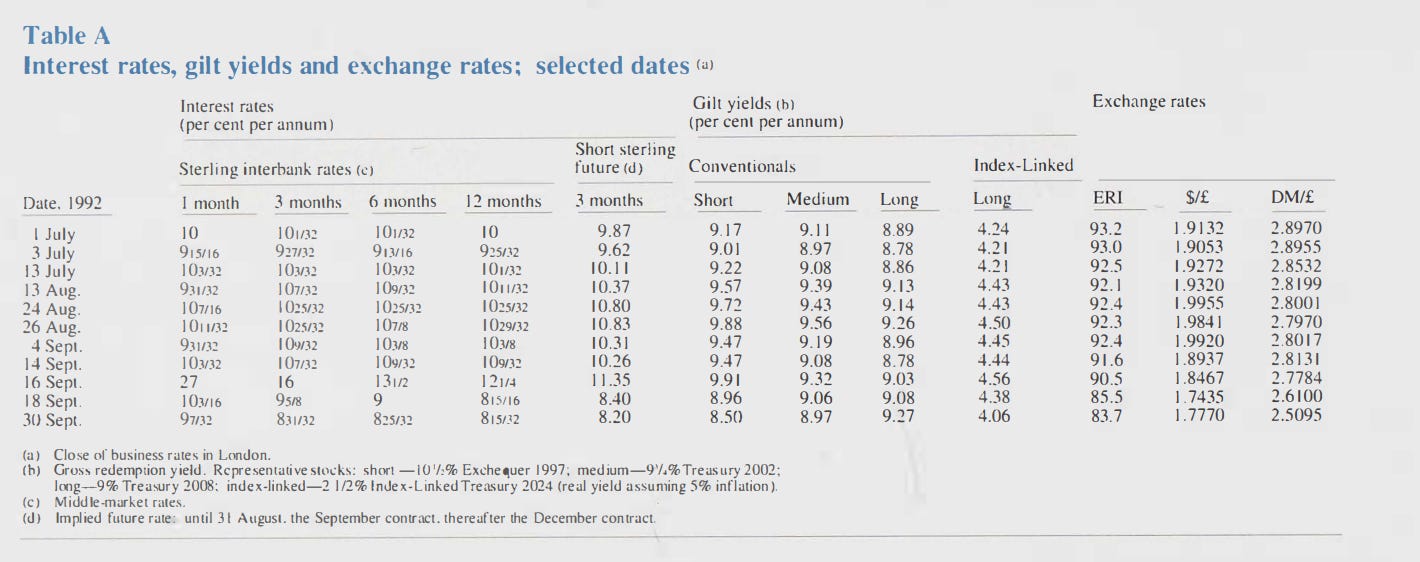

In their efforts to prop up the currency, the Bank of England borrowed at least £5 billion European Currency Units (ECU)—a basket currency that was based on a collection of various European currencies before the Euro—to buy up pounds and keep its value high as well. Soros was quoted saying that the British finance minister was willing to borrow $15 billion to defend sterling. Interest rates would spike to an incredible 27 percent for the day.

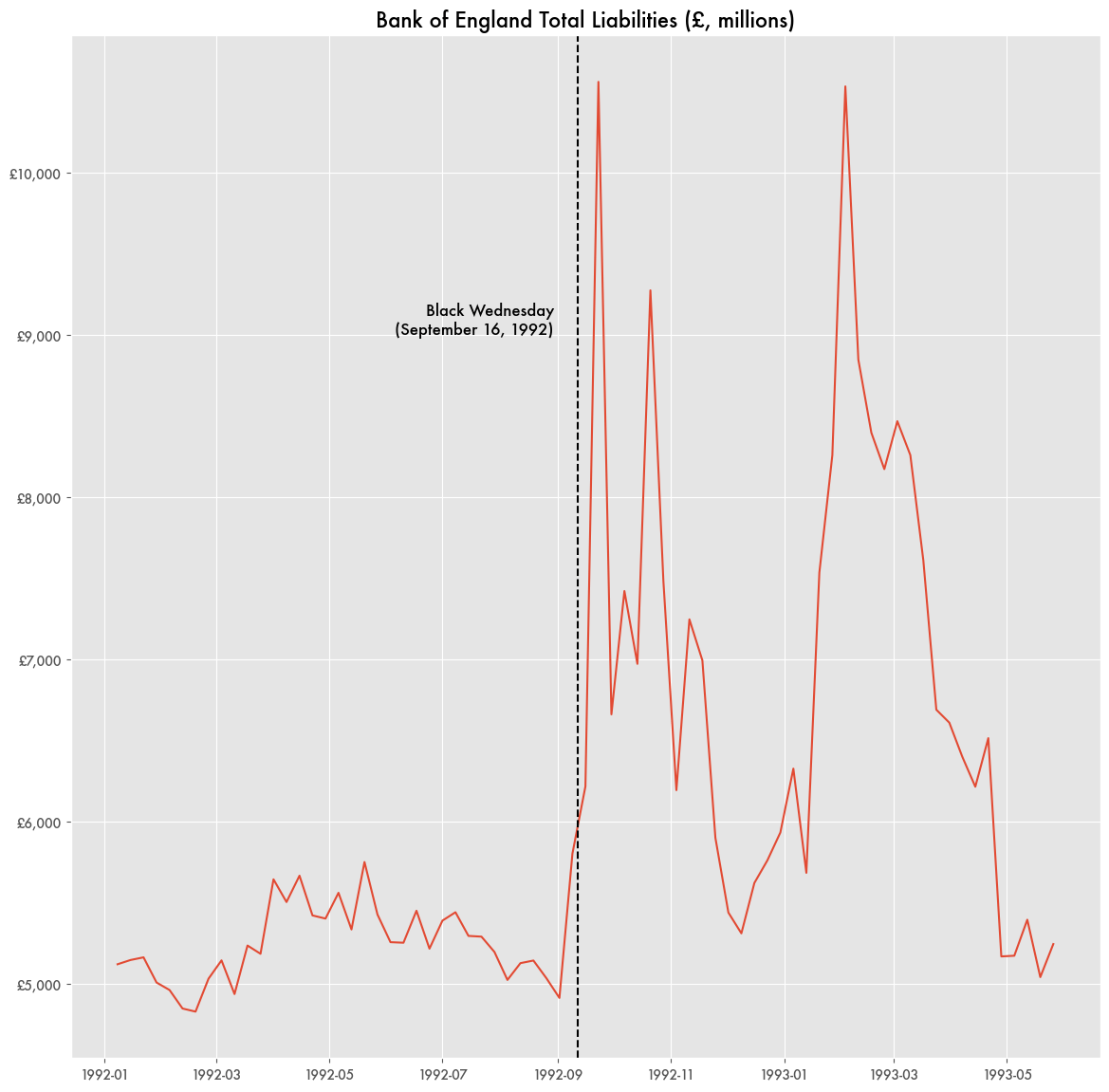

Likely due to that debt, total liabilities for the bank would double within a week, topping £10 billion at a time. While some interviews have described the attempts to prop up sterling as completely ineffective, the value against the dollar would rise by 5 percent in the week leading up to Black Wednesday.

But the fervent effort by the bank to prop up the value of sterling was only temporary, and the U.K. would announce its exit from the ERM as the pound went into freefall.

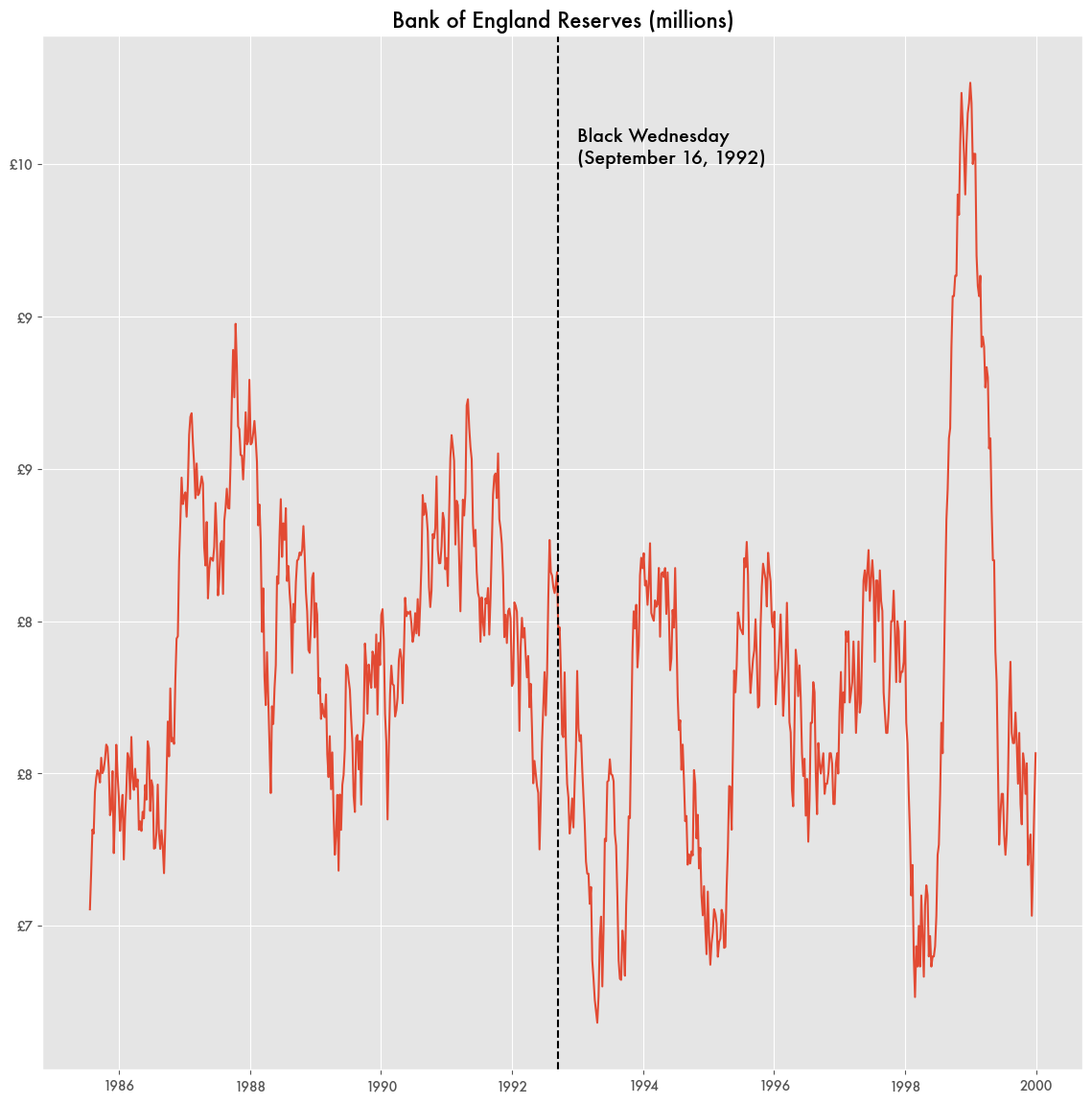

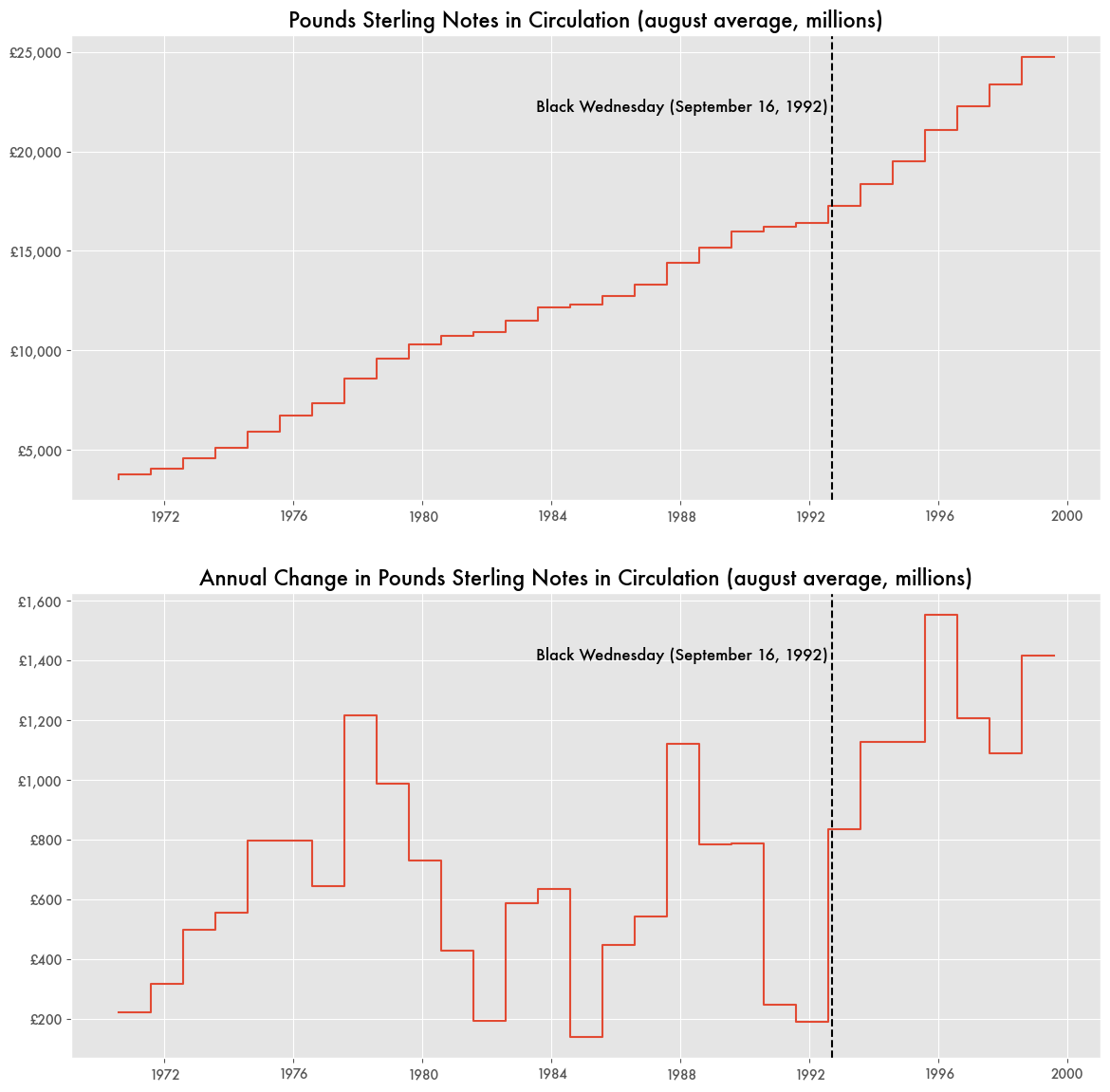

Yet somehow borrowing billions and buying billions of pounds that would lose 20 percent of their value in a matter of days didn’t make much of an impact on the bank’s bottom line. A loss of £1 billion to currency speculators would seemingly stand out in total liabilities. Other anecdotes have put the price at £3.3 billion. But within a month total liabilities were back where they were pre-crisis. It was as if the bank borrowed billions only to immediately pay it right back with no major loss.

Large holdings of currency—whether it be in pounds, ECU, or another currency that the U.K. might have traded for—would ostensibly show up in the total reserves of the bank, but there is no visible sign of billions in debt or reserves left on their books when it was all done.

Devaluation Was Expected

While sometimes Soros’ bet is described as investing genius, the collapse of the pound was not that big of a surprise. Italy and Spain also devalued their currency around the same time when they realized they couldn’t keep up their currency’s value and the ERM was not in their best interests.

For years prior, Britain struggled with the burden of high exchange rates, which made their exports more expensive to the rest of the world. Additionally, high interest rates burdened ordinary borrowers, from local businesses to those trying to buy a house. The idea that Britain would continue to keep their currency value high by raising interest rates even higher just to be a part of Europe comes across as economic suicide.

Some of their strategy was based on the hopes that Germany’s Bundesbank would lower their interest rates, which would in turn cause the pound to be more valuable. But in the days prior to Black Wednesday Germany announced the increase to the country’s interest rates, and it was a measly .25 percentage points for the Lombard rate and .50 percentage points for the discount rate. With that announcement, the collapse of the ERM agreement was all but inevitable.