EPI's Misleading Pay-Productivity Gap

The divergence between average wages and productivity over the last century is sometimes referred to as the “Great Decoupling.”

The Economic Policy Institute (EPI), a union-affiliated think tank, produces a prominent report on the pay-productivity gap, pointing at the 1970s as the era when the U.S. moved away from unions and towards deregulation that likely led to the decoupling. In short, wages haven’t kept up with productivity because workers have less negotiating power.

According to the EPI report, “[worker pay] climbed together with productivity from 1948 until the late 1970s.”

But what the EPI analysis fails to mention is potentially the largest economic change in the U.S. history which would affect wages and monetary value as a whole around that time—abandoning the gold standard in 1971.

The move away from the gold standard would usher in an age of inflation through the 1970s. Adjusting productivity for inflation is substantially different than adjusting average wages, and the two metrics may not be comparable in the way EPI presents them.

Prior to 1971, the value of the dollar was affixed to the amount of gold available. When President Nixon moved the U.S. off of the gold standard in 1971, it allowed more money in circulation, allowing the government to adjust to economic swings and handle jumps in unemployment. And that led to a sharp growth in inflation throughout the 1970s until Paul Volcker and the Federal Reserve forced a recession beginning in 1979.

While wages used to grow with productivity pre-1970, it was largely coincidental. When looking at nominal—or values unadjusted for inflation—both values have gone up continuously, but wages have actually increased at a higher rate than productivity: 616 percent increase for wages versus 156 percent for productivity.

Real values—those adjusted for inflation—diverged because of rampant inflation in the 1970s and the two metrics are adjusted for inflation in very different ways that are not comparable.

Inconsistency of Comparing Productivity and Wages

One issue in comparing productivity with average wages is that productivity is calculated in total across the population, but wages are averaged over the total labor force.

Year over year, more laborers are added to the population and the total labor population is producing more, but that doesn’t mean each individual laborer is producing more on average—something implied in EPI’s analysis.

This is quite visible when looking at aggregate pay—the amount paid to the total labor force as a whole. The amount paid per productivity has only gone up, likely to pay for the growing labor force.

Since 1970, aggregate nominal pay has increased 1,700 percent, while productivity has only increased 167 percent.

Different Adjustments For Inflation

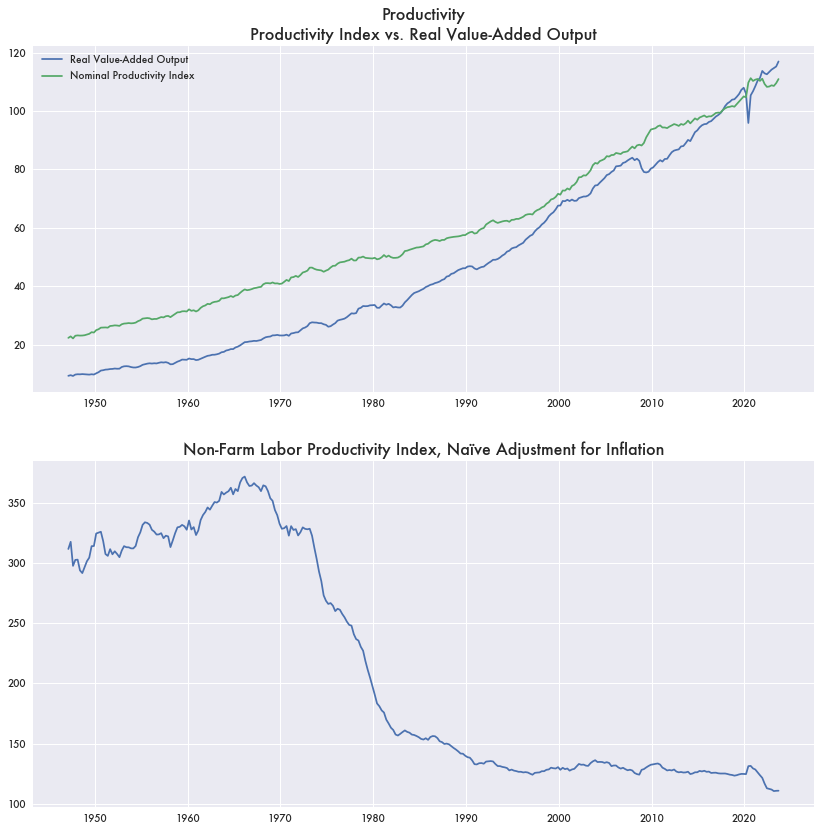

Comparing the two metrics is problematic because it’s a different process to adjust each one for inflation. Real (adjusted for inflation) productivity is usually measured in a “real value-added output” calculation that is substantially different from simply adjusting productivity based on the average cost of goods and the Consumer Price Index (CPI).

Without going into the details of how that real value-added output calculation is made, if productivity was adjusted for inflation in the same way that wages and other economic metrics were using CPI, it would show a massive decline through the 1970s as if the U.S. suddenly stopped producing anything of value. The same volume of goods produced one year would suddenly be worth less the next solely because of changes in the value of the dollar.

Such a slump on paper helped muddy the waters in the 1970s over stagflation—the simultaneous combination of inflation and a stagnant economy.

While on paper the U.S. economy was ostensibly in decline during that decade, real value-added output shows no substantial decline. The growth in unemployment during that time is likely a common remnant of increasing interest rates.

Median Wages

Overall, since the move away from the gold standard and changes in inflation, median wages tend to be flat until a steady increase began around 2000.

Which is to be expected. Businesses often provide workers with wage increases based on inflation.

One major exception is that as women have become a larger portion of the workforce, their median wages have steadily increased going back to the 1970s. While overall wages were relatively flat, through the mid-1990s, median wages for men were actually in decline as wages for women steadily increased.

The growth of women in the workforce complicates wage metrics as most annual averages now show values for family or household income rather than individual income.

For example, BLS numbers for 2023 median weekly wages equates to $61,739.54 annually in 2023 dollars. Based on a 1978 Census report, the median wage for males in 1958 in 2023 dollars would have been $52,425.68—an 18 percent increase to 2023.

But based on real median family household annual income, it’s gone from $42,540 to $92,750 over that same time period—a 118 percent increase.