Glass-Steagall’s Relevance: The Deregulation that Drove the Financial Crisis

The story of the 2007-2008 financial crisis has left out the role of deregulation.

In the wake of the crisis, financial experts dismissed the effect of eliminating banking regulations like Glass-Steagall in media outlets like NPR and the Financial Times since the law was mainly aimed at preventing banks from getting too large or “too big to fail,” which wasn't essential to causing the crisis.

According to former Treasury secretary and chief economist for the World Bank Larry Summers, “virtually everything that contributed to the crisis was not affected by Glass-Steagall even in its purest form.”

But Glass-Steagall was not intended to prevent banks from becoming too large. It was originally created to prevent conflicts of interest between commercial and investment banking.

And with the elimination of Glass-Steagall in 1999 via the Gramm-Leach-Bliley Act (GLBA), and more so with the Commodities Futures Modernization Act (CFMA), it opened the floodgates for new kinds of conflicts via derivatives that would be at the heart of the financial crisis.

Deregulation allowed collateralized debt obligations (CDOs), once an obscure financial instrument, to run rampant with commercial banks now creating and investing in securities that the CFTC was unable to regulate.

Explosion in CDOs

Investment and issuance of CDOs exploded in the early 2000s following a series of deregulatory maneuvers.

According to numbers from the Securities Industry and Financial Markets Association (SIFMA) provided by Numhub, investment in CDOs was practically non-existent prior to 1995. But by 2006, over $500 billion had been issued.

In between, derivatives, lending standards, and bank investing were deregulated in multiple different ways.

Beginning in 1996, the Office of Thrift Supervision (OTS) pre-empted state banks from enforcing certain anti-predatory lending (APL) laws—laws intended to limit abusive or negligent lending such as certain subprime loans.

In 1999, GLBA eliminated Glass-Steagall’s wall between commercial banking and investment banking. And in 2000, CFMA outright prevented the regulation of derivatives.

And in 2004, the Office of the Comptroller of the Currency (OCC) pre-empted state anti-predatory lending laws, similar to what the OTS did eight years earlier. Without those state rules being enforceable, subprime lending was untethered.

According to University of Virginia professor of politics Herman Schwartz, all the changes—GLBA, CFMA, and state APL laws—enabled the CDO market to grow out of control, but CFMA was the most important.

“[CFMA] said that the government just wasn’t going to regulate derivatives, which could have been handled by the Federal Trade Commission (FTC). It enabled an enabled an explosion in CDOs as well as credit default swaps and naked default swaps,” Schwartz told Investigative Economics.

Schwartz also compared naked credit default swaps to stranger-based insurance, where the investor has no beneficial interest in the debt being insured.

“It’s like having a neighbor take a fire insurance policy on your house,” Schwartz added.

Elimination of Glass-Steagall was not as important, but still integral. According to Schwartz’s paper “Finance and the State in the Housing Bubble,” eliminating the firewall between commercial and investment banking allowed banks to bypass Fannie Mae and Freddie Mac—the government-sponsored entities that were given the authority to create mortgage-backed securities (MBSs).

Now banks could create their own MBSs on their commercial side and sell them to investors on the investment side. According to Schwartz, By 2004, "private securitizers were creating more than half of the $1.8 trillion in MBS issued that year."

The potential conflict of interest of a bank selling an investment that it produced is eerily similar to the kinds of conflicts of interest that led to the firewall of Glass-Steagall in the first place.

During the Pecora commission in the 1930s, the government exposed how National City Bank, which eventually became Citibank, sold billions of Peruvian bonds despite the bank knowing that the country was in extreme financial distress and not informing their investors because the bank benefitted from the sales.

Almost 70 years later, Citibank would be instrumental in lobbying to remove the firewall of commercial and investment banking, morphing into Citigroup in the process.

Pre-Emption of State Laws

In the 90s, states like North Carolina had implemented their own anti-predatory lending laws—additional legal protections for borrowers in the mortgage market.

According to a 2009 report from the University of North Carolina’s Center for Community Capital, this included protections against home equity stripping, loan flipping, abusive interest rates and fees, and inclusion of unwarranted prepayment penalties.

But policies pushed by the OTS in 1996 and the OCC in 2004 enabled federally chartered banks to ignore these state regulations.

Without enforcement of those state regulations, banks could make subprime loans as long as they adhered to the less stringent federal standards. Many of those subprime loans would eventually undermine the wide range of derivatives that they were based on: MBSs, CDOs, and CDSs.

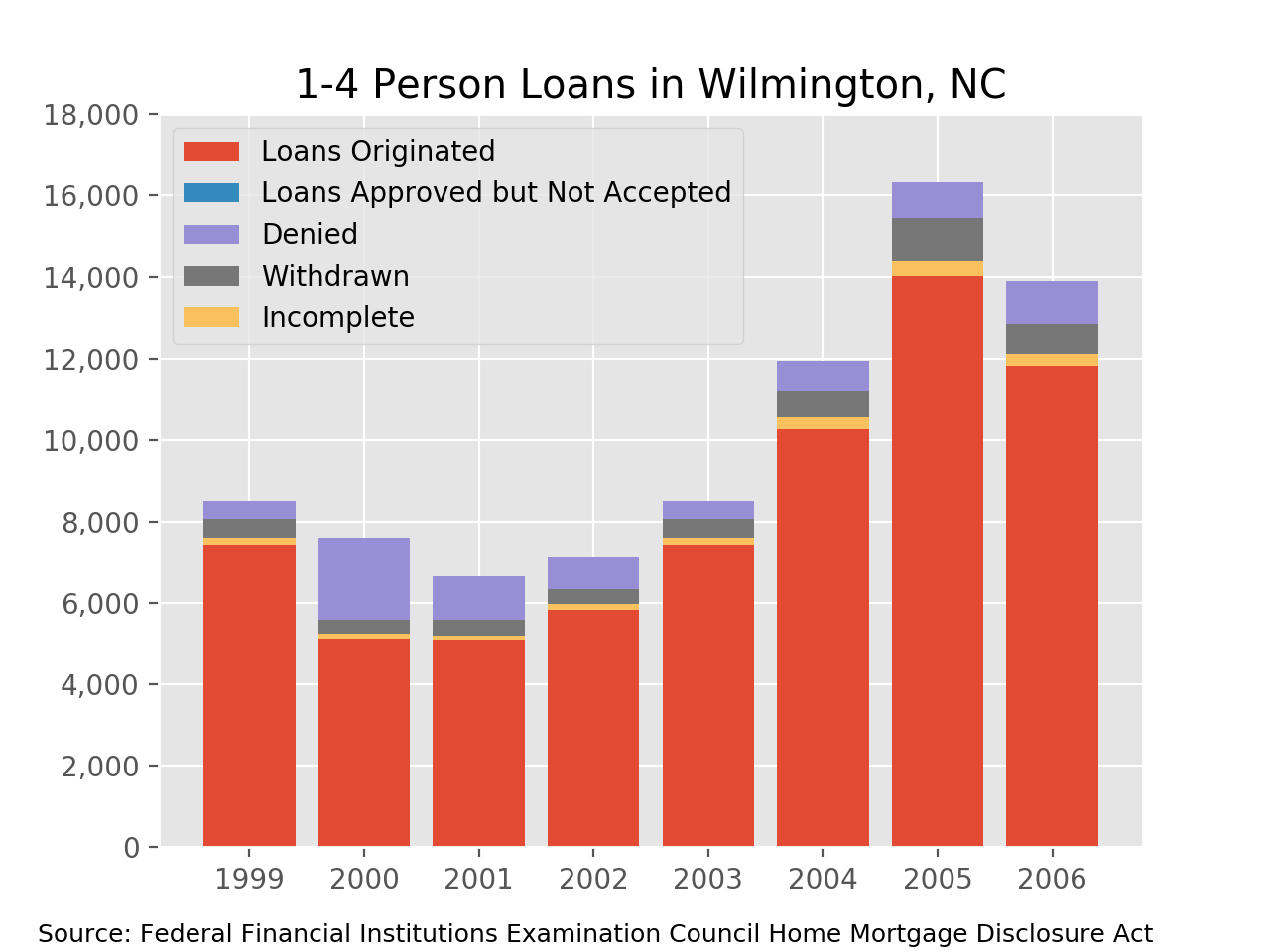

In the example of North Carolina, the state enacted lending restrictions in 1999, which would slightly depress lending in the next few years according to numbers from the Federal Financial Institutions Examination Council (FFIEC).

But by 2006, after the OCC pre-empted North Carolina's lending restrictions, lending in places like Charlotte had doubled from four years prior.

Watters vs. Wachovia

While it wasn’t a deregulatory maneuver, the decision in Watters vs. Wachovia was potentially a last gasp for state banking laws to regulate certain kinds of anti-predatory lending that led to the financial crisis.

The 2006 Supreme Court decision that came within a year of the financial collapse allowed the OCC to promulgate the 2004 rules that pre-empted state anti-predatory lending rules.