Pandemic Exposes the Affordable Care Act's High Costs and Flawed Incentives

One of the ostensible outcomes predicted for the Affordable Care Act (ACA) is that it would drive down health care costs.

More citizens having health insurance would help spread the risk and encourage preventable care. Access to insurance exchanges meant consumers could shop around for more affordable plans.

But premiums have gone up on average. A Kaiser Family Foundation survey put the average cost of family premiums for employer coverage at $13,770 in 2010—or $18,270 in 2022 dollars when accounting for inflation. In 2022, it was $22,463—or 23 percent above inflation.

With higher insurance costs and more people enrolled, the U.S. has gone from having the highest health care expenditures in the world to even higher.

The pandemic’s shutdown of a significant portion of medical care should have led to a significant reduction in spending. But it didn’t. Stipulations in the ACA are meant to ensure all that money goes towards health care, but that requirement may also be encouraging medical providers to charge more for the same procedures.

Largest Health Care Expenditures in the World

Even before the ACA, the U.S. easily spent more per capita on health care than any other country in the world in terms of international dollars—a fixed-value pseudo currency used to compare spending from one country to another—based on World Bank data.

That’s far beyond what other wealthy countries at the top of the list spend, like Luxembourg, Switzerland, Norway, and Germany. In 2011, the U.S. spent $2,239 more per person (38 percent more) on health care than the next largest spender, Switzerland.

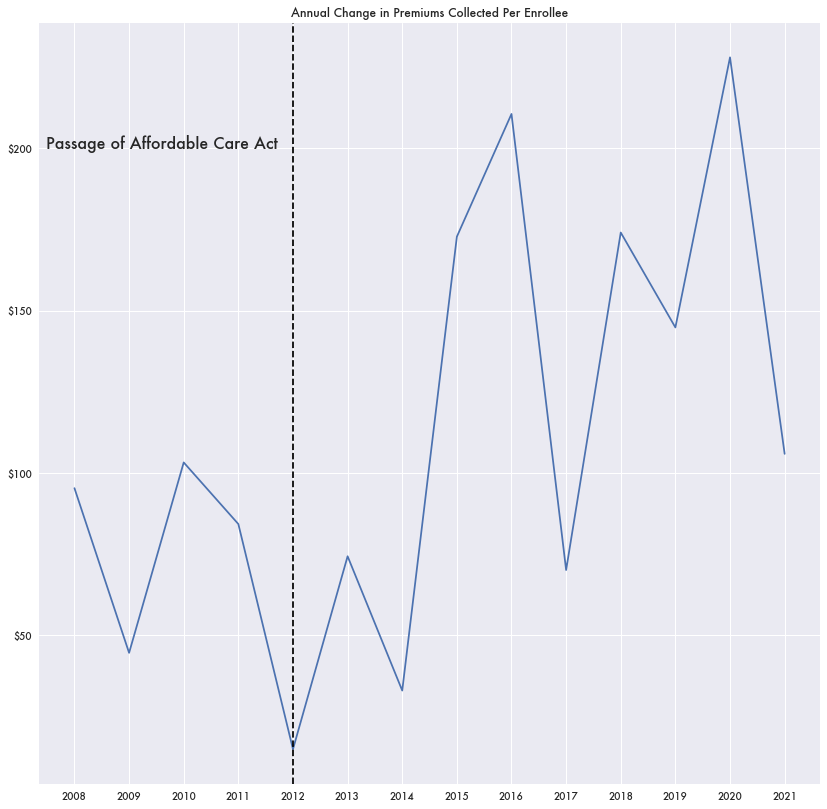

Growth in Spending Since ACA

Before the ACA, health care spending by the government, insurers, or individuals tended to increase year-over-year with inflation.

But that growth has doubled since 2014. What was on average an increase of $235 per capita a year in international dollars from 2008 to 2011, it would become $400 a year from 2014 to 2019 based on data from the National Association of Insurance Commissioners (NAIC).

Some of that was to be expected. More enrollees and more government spending and more government subsidies would lead to more more people having health insurance, more money paid into insurance plans, and more money spent on health care.

But the amount of insurance premiums collected per enrollee by itself has gone up. That is, insurance costs have gotten more expensive—not just that more people are enrolled.

What was at most a growth of $100 per year in premiums per enrollee before 2014 would double by 2016.

Medical Loss Ratios

Spending stipulations as part of the ACA require that insurers spend no less than 80 percent of their premiums on medical care (85 percent for group market plans)—otherwise known as the medical loss ratio (MLR).

That is, they need to spend a certain amount on medical care rather than administrative costs or shareholder returns. Otherwise the insurers need to refund the difference as a rebate to consumers.

But a potential side effect of the MLR minimum is that it may work against the intentions of the ACA: to keep medical costs and premiums down.

There is no benefit to a health insurer keeping their spending down if they are already below the 85 percent threshold. That money will have to be spent as either medical care or as rebates either way. There’s no incentive to negotiate prices with health providers in that situation.

In general, insurers appear to have held to that 85 percent rate minimum, but the decline in health treatment during the pandemic led to low MLRs across the board. Sometimes ratios were in the high 50s, like in Kansas, Idaho, and West Virginia. Puerto Rico was the exception. The island had an MLR of a whopping 228 percent in 2020.

High Spending During the Pandemic, Little Utilization

With less health care provided and MLR rate below the threshold, insurers would have to pay out rebates. In total, 2020 would see a large payout of MLR rebates—over $2 billion across all markets according to Centers for Medicare and Medicaid Services (CMS) data.

While $2 billion in rebates is a lot, it’s less than the rebate payments in 2019 ($2.5 billion). And it’s not much considering how much was being brought in via insurance premiums. Collected premiums in 2020 were $73 billion more than in 2019.

While insurance companies were collecting ever-larger premiums and medical spending was at historical highs, hospital utilization was significantly down.

Data from the Agency for Healthcare Research and Quality (AHRQ) Healthcare Cost and Utilization Project (HCUP) shows a distinct drop of around 8 percent in the number of hospital treatment records in 2020 as medical providers and patients postponed non-essential treatments.

An 8 percent drop in medical spending from 2019 to 2020 would equate to $582 billion fewer expenditures based on NAIC data. Much higher than the $2 billion in rebates paid out.

Despite the lack of hospital utilization, Medicare spending per enrollee in 2020 was only down 8/10ths of a percent based on data from Centers for Medicare and Medicaid Services (CMS) National Healthcare Expenditure (NHE) data. Medicaid spending was down one percent, and private healthcare spending was down 2.7 percent.

Either insurers were paying a substantially higher cost for medical services in 2020, or some of the numbers aren’t right.

There may be some evidence to the latter. A 2021 report in the Journal of Insurance Regulation estimated that insurers could be intentionally adjusting medical claim payout data—around 2.3 percent of payout claims—to avoid going below that MLR minimum and paying out rebates.