Financial Crisis Post-Mortem: TARP Mortgage Beneficiaries Were Largely Not Subprime

During the mortgage crisis, foreclosures spiked to an all-time high, driven by increasing interest rates on subprime adjustable rate mortgages.

To stem the tide of foreclosures, President Bush signed the Troubled Asset Relief Program (TARP) in 2008 to aid homeowners struggling to pay their mortgages, as well as other failing business like American Insurance Group and automakers. Eventually the program would spend over $431 billion on the program according to the Congressional Budget Office (CBO) in 2012, but the majority of that went to financial institutions—$313 billion at the time of CBO’s estimate.

Approximately $16 billion went to homeowners through TARP’s Home Affordable Modification Program (HAMP), which would help homeowners struggling to make payments and avoid default modify their loans to something more manageable, such as lowering interest rates or monthly payments, by covering the loan modification costs. Originally HAMP was set to disburse $50 billion, but a portion of funds were disbursed to other loan programs.

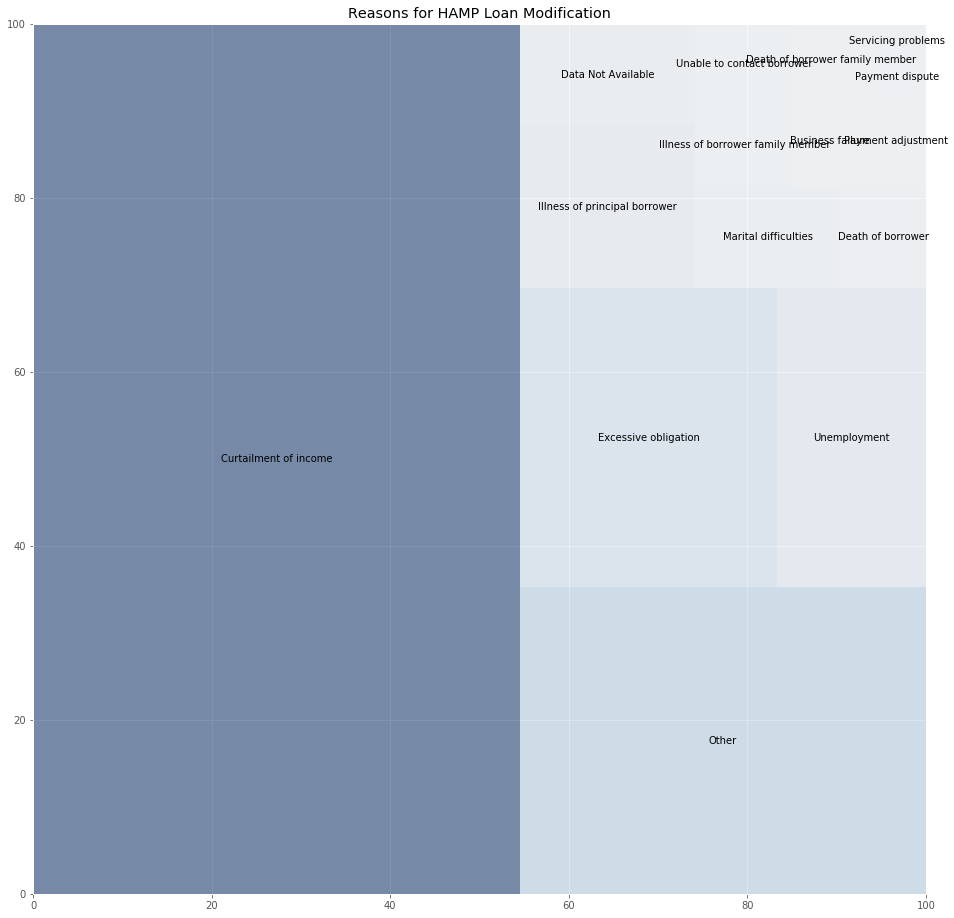

Yet the vast majority of those who applied for loan modifications through HAMP didn’t show the main hallmark of the subprime market at the time: an inability to pay because of excessively high payments on high interest rate loans.

Data on HAMP’s disbursement shows the largest reason stated for applying for the modifications by far was a loss of income: either via unemployment or simply “curtailment of income,” together accounting for 60 percent of applicants. Excessive obligation accounted for about 10 percent of applicants, with other reasons like illness, servicing issues, or “unknown” being less likely.

Few had excessively large interest rates before the modification. Over 98 percent had interest rates less than 10 percent and the larger majority having rates between 5 and 7.5 percent: far away from anecdotal accounts of excessively high rates in the 20s, 30s, or higher for subprime loans with adjustable rate mortgages.

HAMP is known to have had issues. A 2010 report by Special Inspector General for the Troubled Asset Relief Program (SIGTARP) noted that the program originally aimed to make 3 to 4 million loan modifications, then adjusted that to offer 3 to 4 million loan modifications. A 2019 GAO report listed the total at 1.7 million.

Another SIGTARP report listed the re-default rate of the oldest HAMP cohort (from 2008-2009) at a surprisingly high 46 percent and identified that re-default rates for all cohorts were increasing with time rather than declining.

Little Data on Location of Beneficiaries’ Homes

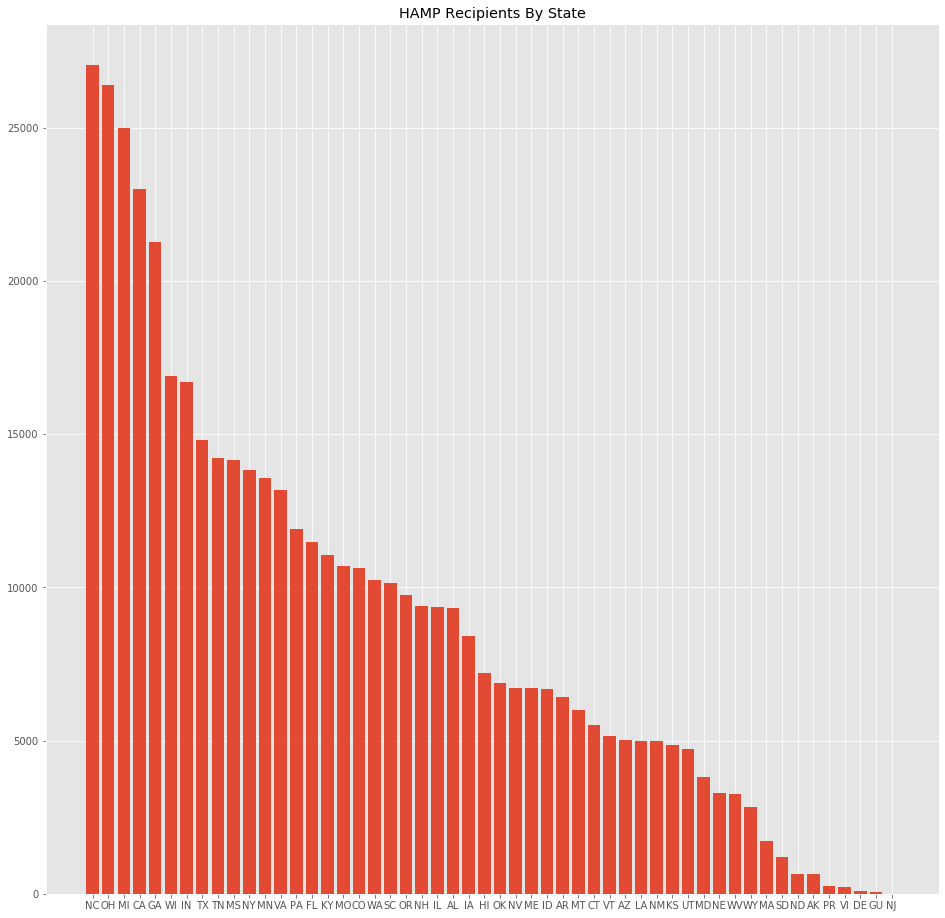

While the HAMP dataset is relatively robust, one field is largely missing: the state of the applicant's home. Ninety-three percent of the data is missing the state where the home resides.

While data on the applicant’s region is there, with the South Atlantic as the most common location (1/4 of all applicants live there), there's no detail as to whether the numbers are dominated by Florida, North Carolina, or another state in the Southeast.

Of the available state data that does exist, North Carolina had the most applicants, with Ohio, Michigan, and California following.

Neither North Carolina, Ohio, or Michigan are known for bearing the brunt of the foreclosure crisis.